AI Second

Can Companies Become AI-Native?

TLDR: Many of my summer dog walks have been occupied by a simple idea: enduring companies in the AI Era don't have to start as tech companies; they can become them.

I call this the AI Second thesis. It runs counter to the dominant Silicon Valley narrative that, to win in this market, you must build from first principles with "AI-native" DNA from day one. There are cases where this will be true. But it ignores a vast swath of the real economy.

Valley Orthodoxy and AI

One of the blessings of living in the Bay Area is direct access to the frontier of technological progress. The downside is that it becomes easy to focus myopically on technology (and venture capital) as the skeleton key that unlocks all commercial opportunities.

This is a real-world manifestation of William Gibson's classic comment that "the future is already here - it's just not very evenly distributed." The actual expression of AI in commercial contexts will likely follow a similarly jagged trajectory, as behaviors and products that are common here take longer to surface at scale elsewhere.

Some AI-first newcos will invent entirely new categories, or transform domains like codegen almost overnight. Beyond that, though, many industries, roles, and business models will evolve more gradually. It is in these areas that the AI Second thesis is most relevant.

Defining AI2

AI Second (AI2) companies are businesses that build a valuable human service first and layer in automation second to improve quality, speed, or cost.

For these companies:

Trust precedes tech.Cashflow funds experimentation.Domain expertise guides automation to the repeatable foundation.

This idea is particularly powerful for Services companies that have earned trust and command premium prices in their domain. Their operators have tacit and deep knowledge, often with extensive nuances that don't show up in current AI training data and are thus hard for generic AI to replicate today.

There is a clear opportunity for these companies to implement AI, even if the technology remains invisible to customers for now. This resonates with the framing, about which I’ll write soon, that the white-collar sector consists of a substantial amount of "knowledge work" that is well-suited to automation, including the digital busywork that we all know well. What remains might be better conceptualized as wisdom work, which is the province of experienced humans who have the accrued experience, taste, judgment, and savvy that human customers value highly.

Shape-Shifting Services

AI2 companies must adopt automation quickly and deeply in the undifferentiated areas of their business. They must also redeploy some of their free cashflow into AI R&D and POCs, some of which will fail. The advantage that these companies still hold over most pureplay software competitors is intangible and human: their deep integration into their clients’ worlds and workflows.

This moat won’t last forever. Those who don’t attempt to become a hybrid Services & Software company will ultimately be outcompeted as underlying AI models get better and new entrants develop their own domain expertise and customer relationships. If you've read prior Gravity Shackles posts, you'll know that I view these Services x Software businesses as increasingly interesting and investable.

You'll also know that the Valley playbook for AI "transformation" has been to start with a tech asset and then to either replace or purchase existing services businesses (e.g., seed-fund a tax automation product, and eventually buy a tax prep firm). There is merit to this approach, but I remain particularly interested in the inverse idea that one can start with the services business and move into technology. Ironically, it is well-known but largely unspoken that much of the “annual recurring revenue” for AI companies today is actually coming from professional services work. In recent days, OpenAI has leaned even more explicitly into its nascent “Palantir-like” consulting business.

There is no shortage of execution and organizational risk in doing the Services & Software work well: staffing in-house or sourcing the right partners, building a productization muscle, risking revenue cannibalization, challenging legacy customers, and motivating the core team to evolve. But it’s viable. The crux is distinguishing between automation that saves time and cost, and automation that generates compounding operating leverage. Companies that do both will be rare and highly valuable.

I've already seen this done across several categories, including a deep learning consultancy that automated many of the rote human-led steps of therapeutics R&D for pharma companies, and a software development firm that compressed the time from initial discovery call to MVP from 90 costly days to 5 hours by productizing the flow from discovery call transcription to PRD generation to automated MVP build and deployment. In both cases, these were existing services businesses that knew the most painful and valuable bottlenecks, and used technology to transform their service delivery.

Becoming a Cyborganization

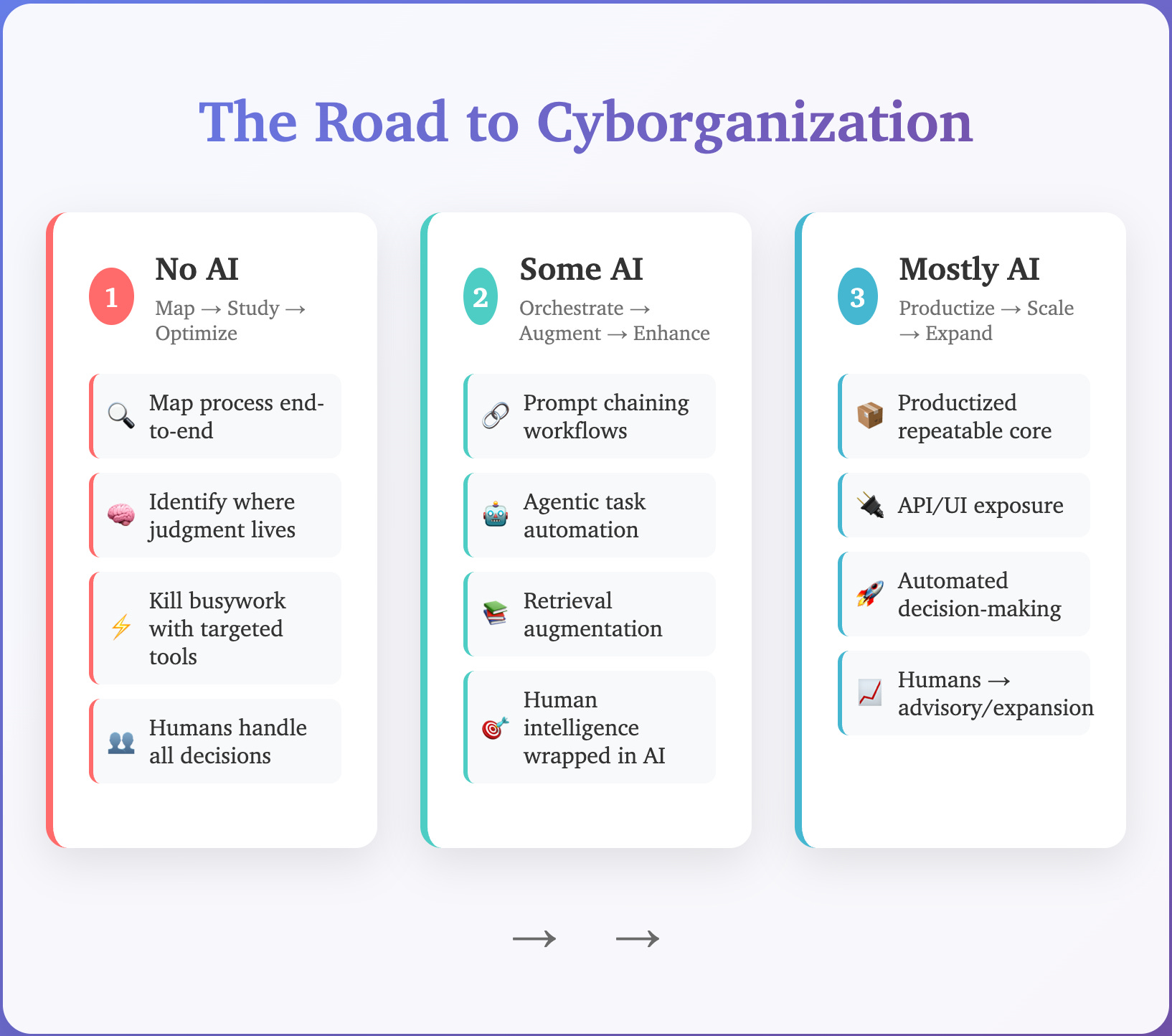

Yes...time to road-test a new name for these "cyborg" corporations that are neither pure services nor pure software. The dynamics of this transition can be thought of simplistically in three sequential steps.

No AI: Map what humans do inside the company. Study where to draw the line between knowledge and wisdom work. Decide what to automate and in what order.

Some AI: Wrap remaining human components in lightweight AI orchestration: prompt libraries, internal assistants, basic agentic workflows (mostly non-customer-facing), RAG-connected knowledge bases. Run POCs. Migrate winners to production.

Mostly AI: Productize the repeatable core. Expose it via UI, API, or invisible human assist. Redeploy humans to higher value work, innovation, and net-new opportunities. This is when inorganic growth through M&A makes the most sense.

By the time a firm reaches Stage 3, the line between "services" and "software" blurs enough to be commercially irrelevant. Margin structure improves, valuation multiples shift, and new pricing models and customer segments are unlocked. And, ideally, every incremental project is generating data or other value that reinforces the stickiness and quality of the service in question.

Much has been written about related and contrasting ideas, particularly as the "AI rollup" thesis has picked up steam in recent months. Ultimately, there is no shortcut to the outcome; it will take time before we have real examples of how these different strategies compare, and the successes and failures along the way.

I believe the “AI Second” thesis is one of the less-explored (and more promising) paths in today’s market. In the coming months, I’ll share more from time spent with these companies off-screen and in the real world. Stay tuned.